Yesterday, I mentioned an interesting ‘find’ about Emmett’s medical history — more specifically — his cause of death.

The official record states ‘uremia’ (chronic kidney failure) as the cause of death. Although there were other related issues going on with him, the bottom line is that Emmett’s kidneys shut down, and that is what killed him. Other than palliative treatment, if you had chronic kidney failure in 1918, there was nothing anyone could do for you. Transplants and dialysis were decades off. Still, I’ve always found his death of kidney failure worth investigating in detail.

From what I’ve learned after talking with medical experts and studying current (as well as early 1900) medical literature, one didn’t just get kidney failure suddenly. Uremia was and is a slow-moving, chronic disease, with very real, uncomfortable symptoms. Also, kidney disease typically comes about because of another pre-existing, underlying condition, usually high blood pressure, diabetes, or nephritis, for example.

Physicians knew the connection between high blood pressure and kidney failure, even during Emmett’s time, according to the medical literature. I have found articles in medical journals dating back to the 1890s corroborating this. Unfortunately, not every physician checked a patient’s blood pressure regularly.

Based on this (and other previous research), I’ve come to the understanding that Emmett, very likely, had early onset high blood pressure, that was undiagnosed or, misdiagnosed, and it wasn’t discovered until after he experienced complete kidney failure in December, 1914.

Sphygmomanometer, 1910.

Believe it or not, it wasn’t the physicians or the AMA back then that had pushed for blood pressure monitoring as part of routine patient checkups.

It was the life insurance industry.

Life insurers wanted to keep payout costs down; so, in 1910, before anyone could have a policy written for them, they had to have their blood pressure measured. And, the insurance companies provided sphygmomanometers to their trained medical consultants, who would measure the policy holder’s blood pressure at his or her office, or home, or wherever it was convenient.

There was quite a bit of published research on blood pressure measurement and its connection to heart attacks and kidney failure in patients existed. The insurance industry used that to their advantage. But what about the physicians?

Despite the known benefits of measuring patient blood pressure, there were reasons why it was not standard practice among general practitioners to check a patient’s blood pressure.

First, not every doctor had a sphygmomanometer at his or her disposal. The literature reveals that physicians, especially rural ones, could not afford them.

Also, according to the literature, not everyone used a sphygmomanometer correctly, and so inaccurate readings were a problem. (Before these devices came along, measuring blood pressure was an invasive procedure.)

Finally, it simply wasn’t a ‘regular’ step in every doctor’s examination routine. There are several articles published in medical journals for 1912 arguing for blood pressure measurement as a routine step in every basic patient examination.

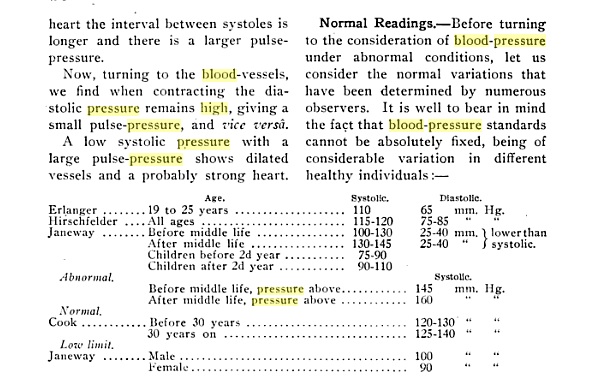

There was no one standard for a healthy blood pressure reading in 1912. Source: Sajous, 1912.

More significant, though, is the fact that there was not yet a consistent, set measurement defining high blood pressure in the medical industry.

“Acceptable” blood pressure measurements for an adult Emmett’s age could range between 110 to 140 systolic; one insurance company was using 170 systolic as an acceptable reading in some adult populations. (Today, anything below 120/80 is considered a healthy blood pressure reading for adults.) So, doctors didn’t have a standard, vetted measurement to use in catching dangerous blood pressure readings in 1912 — I can see why some might not check the measurement as a standard of practice if it was not established.

There were also situations where soft-hearted insurance agents would ‘fudge’ some of the blood pressure readings to allow their friends a life insurance policy. Finally, depending on who you were, other insurance companies would forego the blood pressure requirement.

Emmett took out his life insurance policy in 1912, after he had won election to Congress. Coincidentally, Emmett had just finished successfully defending this particular life insurance company in an important lawsuit, saving the company from having to pay a former policy holder about $50,000 in 1912 dollars.

I have a feeling the insurance company either excused the blood pressure examination requirement for Emmett, or, if the life insurance company medical examiners read his blood pressure, it was high (by today’s standards, not 1912 standards), and the medical examiner decided to let Emmett have the policy anyway, because of who he was and the legal work he did for the company.

Regardless, I think Emmett’s high blood pressure could have been caught back then, and if it had, it could have saved his life.

More to come on this subject. Stay tuned.

Categories: Congressman Family Research Status

jsmith532

Professor,

Communication, Arts, and the Humanities

The University of Maryland Global Campus

Leave a comment